CHAPTER 2 THE BUSINESS OF IMPLANT DENTISTRY

History

History Growth

Growth

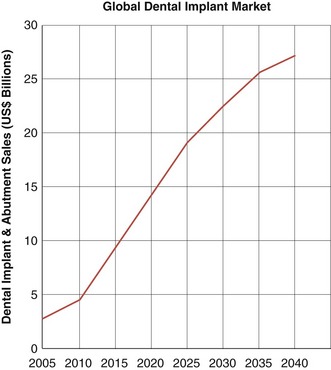

Dental implants were just one segment of a $92.8 billion global dental services market for 2007.1 Global sales of dental implants and abutments rose more than 15% in 2006 alone, reaching $2 billion (Figure 2-1). The growth was strongest in Europe, where sales peaked at $750 million, which was 42% of the global market.2

Fueled by strengthened patient demand, interest in offering dental implant surgery increased among general practitioners. The market projects to continue double-digit annual growth though 2012.3

Volume for dental implants in the United States in 2008 was projected by Millennium Research Group to be 1.4 million procedures, for a treatment value of $2.3 billion. Projections show that by 2012 there will be 4.5 million implants and more than 2.8 million procedures annually in the United States.4

New Investment

New Investment Patient Demand

Patient Demand

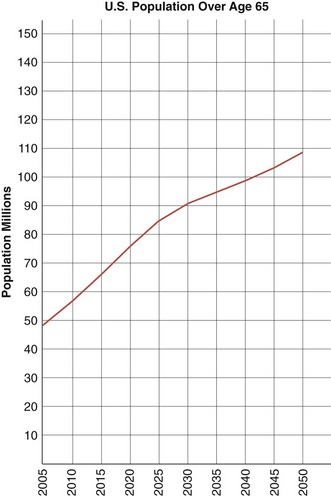

Tooth loss is most pronounced among the elderly, and data show the population in developed countries is aging and will continue to do so. In the United States, the baby-boomer generation is the major purchaser of elective plastic surgery and antiaging remedies. Boomers are the most affluent older generation ever in the United States and they will inherit the largest inflation-adjusted transfer of wealth in history: $10 trillion.5 Their propensity for discretionary spending has fueled remarkable growth in implant dentistry during the last decade. This boomer generation will swell the 65-year-plus population in the United States at annual rates of 1.5% to 3% from 2010 through 2035. Those older than 65 will increase from 12.4% of the population in 2000 to 20.6% in 2050 (Figure 2-2).6

Figure 2-2. Population growth of U.S. residents over the age of 65 from 2005 through 2050.

(From the United States Census Bureau.)

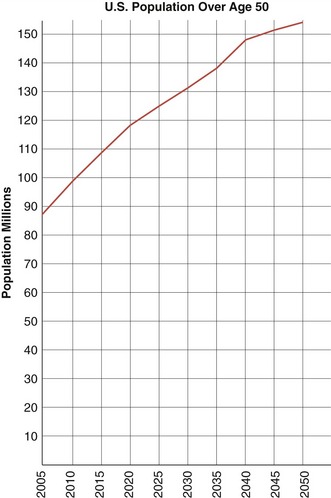

Boomer-related implant growth can be counted on for at least another decade (Figure 2-3). Currently, implant market penetration in the United States is only 2%, according to Dr. Michael Sonick of Connecticut, writing for Contemporary Esthetics and Restorative Practice in 2006. That translates to 3.5 implants per 1000 people.7

Figure 2-3. Population growth of U.S. residents over the age of 50 from 2005 through 2050.

(From the United States Census Bureau.)

Worldwide, dental implant costs vary widely. As of 2008, implants in the United States averaged $1800 in addition to the cost of a crown, and the cost of full-mouth reconstructions with implants started at $12,000 per arch.8 In the United Kingdom the price of a single-tooth implant, including prosthetics, was generally $2,000. In Turkey, it was $800.

A 2005 Millennium Research Group study showed that the U.S. market accounted for $370 million in dental implant sales, with an annual placement of 800,000. The average patient had two implants placed. Based on an average implant fee of $1500, the total 2005 dental practice revenue stream from placing implants was $1.2 billion, with an additional $1.2 billion in restorative revenue for a total of $2.4 billion. In 2007 the total number of implants placed in the United States was 1.7 million.9

Dental Implant Practice Growth

Dental Implant Practice Growth

As the trend toward mainstream status for dental implants continues, more general dentists will include implants as a core offering, especially for single-tooth replacements. Increasingly, they will be prodded by patients who desire a wider range of services. A 2007 survey from The Wealthy Dentist showed that 53% of general dentists in the United States offered the restoration of implants to their patients.9a Many qualified their answer by adding that they accepted straightforward cases but referred their more difficult cases to specialists.

The number of general practitioners in the United States surgically placing implants has not increased at a rate to match the expansion of the implant industry. Some dental schools have responded by adding implant treatment to predoctoral programs. Estimates place the numbers of dentists worldwide who offer dental implants at 140,000 out of approximately 940,000, or 15%. That percentage is projected to climb gradually, to as high as 40% by 2040.10

Costs and Overhead

Costs and Overhead

“One of the problems for the general practitioner,” says Dr. Charles Blair, a dental practice consultant in the Charlotte, NC area, “is that the crown/custom abutment and implant index for laboratory cost can be quite high.” 11 The patient cost of a complete single implant crown, including surgery, can easily be in the $3000 range.

Dental Laboratories

Dental LaboratoriesStay updated, free dental videos. Join our Telegram channel

VIDEdental - Online dental courses