Although some offices may still perform these tasks manually, the use of computer software will provide the practice with the benefits shown in Box 16-1. The administrative assistant must have a basic understanding of the software system involved. All financial activities can be performed online via the Internet in most modern practices.

When processing financial documents, accuracy is essential. The verification of data and attention to detail are necessary to ensure that the processed information is accurate. Incorrect data can mean improper cash flow analysis, inaccurate accounts receivable, erroneous claim form preparation, and inaccurate budget and expense figures. All of these can have very serious repercussions for the entire business.

Practice Note

Practice Note

When processing financial documents, accuracy is essential. The verification of data and attention to detail are necessary to ensure that the processed information is accurate.

As the administrative assistant becomes more skilled in the business office, his or her responsibilities will probably include completing many monthly and annual forms vital to the dental practice. This chapter presents the major types of financial systems and the data that must be processed and managed in a modern dental practice. The chapter shows how technology is applied to the financial operations of a practice to make it more productive. In addition, it discusses the resources available through the Internet that can act as guides for procuring and filling out many of the financial forms needed by the practice.

Determining a Budget

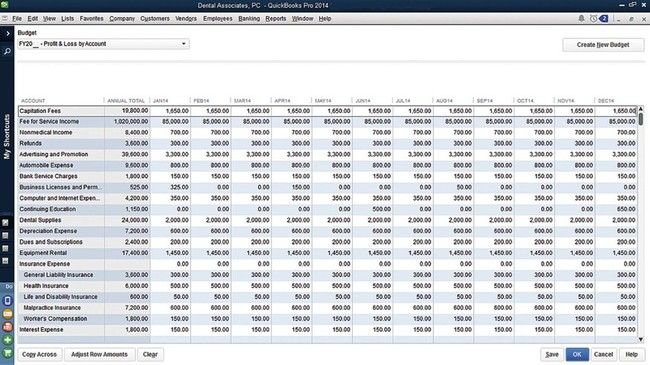

A budget is a dental practice’s financial plan of operation for a given period, usually 1 year. The purpose of the budget is to establish the practice’s financial goals. To achieve an acceptable level of profit, expenditures (the amount of money spent to operate the practice) must be kept in balance with revenue (the amount of income received by the practice). Dentists can use spreadsheet software to develop a budget so that they can plan more thoroughly and in less time than with paper-and-pencil methods. Spreadsheets allow planners to see how a change in one calculation affects all of the related calculations. A template of a business budget created in QuickBooks software for a dental practice is shown in Figure 16-2.

Bank Accounts

One of the daily routine functions of the dental office administrative assistant is the control of the cash flow, which is the amount of money received and the amount disbursed. Although this is being accomplished electronically in most practices today, a good understanding of banking technology and procedures is necessary. Some of the administrative assistant’s banking responsibilities are check writing, accepting checks from patients for the payment of services, endorsing and depositing checks, keeping an accurate bank balance, and reconciling the bank statement; these may be done manually or electronically.

Practice Note

Practice NoteOnline Banking

For many dental offices, electronic or online banking means 24-hour access to cash through an automated teller machine or the direct deposit of paychecks and accounts receivable into a checking or savings account. Electronic banking now involves many different types of transactions. For example, the federal government is even moving toward the direct deposit or transfer of funds for employment taxes as well as for the many other government forms required to conduct business.

Online banking makes use of a computing or mobile device and electronic technology as a substitute for checks and other paper transactions. Electronic fund transfers (EFTs) are initiated through devices such as cards or with codes that let the dentist or those authorized by the dentist access an account. Many financial institutions use automatic teller machines (ATMs) or debit cards and personal identification numbers (PINs) for this purpose. Other institutions use devices such as debit cards or a signature or scan to access to an account. The federal Electronic Fund Transfer Act (EFT Act) covers some electronic consumer transactions.

ATMs or 24-hour tellers are electronic devices that allow banking to occur at almost any time. To withdraw money, make deposits, or transfer funds between accounts, an ATM card is inserted, and a PIN number is entered. Generally, ATMs must indicate if a fee will be charged and then provide the amount of the fee on or at the display screen before the transaction is completed.

Direct deposit enables a person to make a deposit to an account on a regular basis. With this system, the dentist may preauthorize recurring bills to be paid automatically; such bills may include insurance premiums, mortgages, and utility bills.

Online banking allows the account to be accessed from a remote location, such as the office or a personal computer. The account holder can view the account balance, request transfers between accounts, and pay bills electronically.

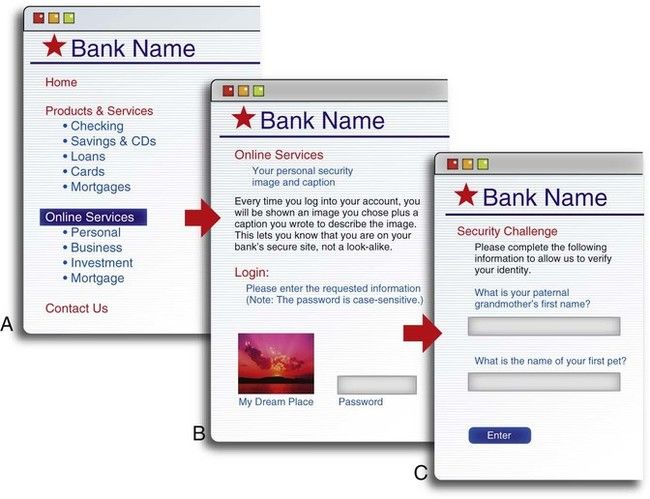

The use of electronic transfers should be monitored carefully. The dentist and any other person responsible for electronic banking must read the documents that are received from the financial institution that issued the access device. No one should know the PIN except the responsible person or persons. The steps that are common to accessing an account are illustrated in Figure 16-3. Each bank will set up some form of security system to verify that an authorized person is accessing the account.

Before any electronic transfer system is used, the institution must provide the following information, which should be filed:

If problems arise in the use of online banking, a complaint can be filed through the website for the state member banks of the Federal Reserve System at www.federalreserve.gov.

Establishing a Checking Account

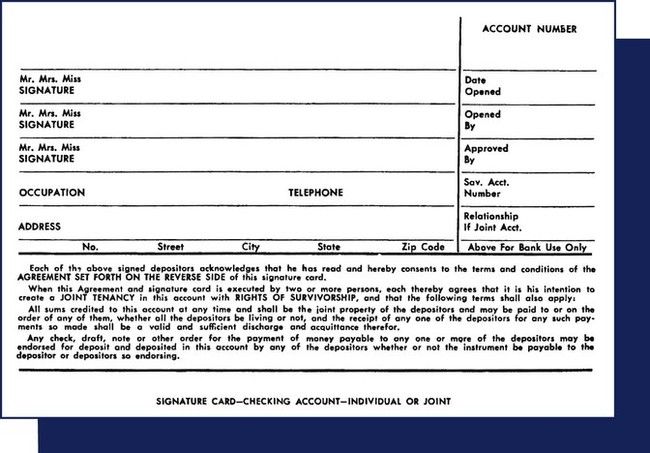

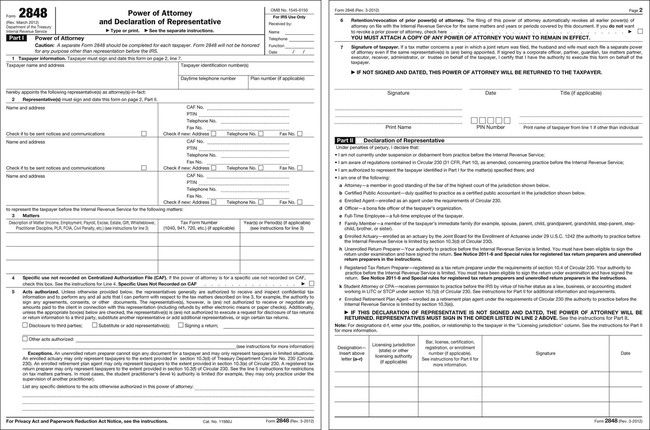

As a rule, the checking account for the dental practice will have been opened before the administrative assistant begins working for the practice. However, when opening the account, the dentist had to decide what type of an account would be used: either a traditional manual account or an account with online access. The dentist also signed a signature card (Figure 16-4) that permitted him or her to write checks against the account. If another person is permitted to process transactions against the account, that person’s signature must also appear on a signature card for the account or on the same signature card that the dentist signed. However, if the administrative assistant is allowed to sign the checks, the bank may require that the assistant be given power of attorney (Figure 16-5).

Checks

Checks are a means of ordering the bank to pay cash from the bank customer’s account. In the past, checks accounted for a majority of all financial transactions in the United States. However, the use of online banking and debit cards has risen dramatically. Patients increasingly will use debit and credit cards rather than cash or checks to pay their bills. However, checks still constitute a significant portion of the receipts for the dental practice.

Practice Note

Practice Note

Debit cards and electronic transactions have decreased the percentage of financial transactions in this country done by check.

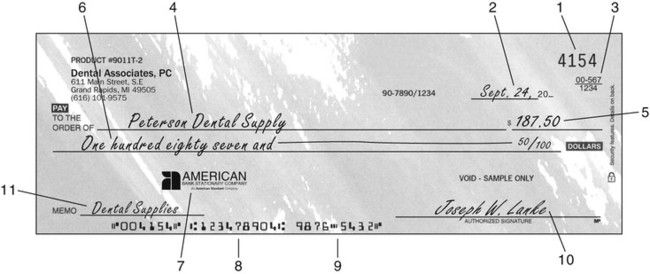

Many parts of a check are self-explanatory; however, some parts need additional explanation. In Figure 16-6, the number 3 indicates the American Bankers Association (ABA) bank identification number. With this coding system, every bank is given its own number, which constitutes a numeric name for the bank. This number aids the sorting of checks for distribution to their proper destination. The ABA number is a fraction, and it is usually printed in the upper right corner of the check or slightly to the left of the check number. The number 4 in the figure indicates the payee, which is the individual or company that will receive the money. The number 7 indicates the drawee, which is the bank that pays the check. Numbers 8 and 9 indicate magnetic ink character recognition (MICR) numbers. These are encoded on all checks to facilitate high-speed handling by machine. The first number is the bank identification number (also found in the ABA identification number), and the second number is the check writer’s checking account number. These numbers can easily be read by people or by machine. The number 10 indicates the signature of the drawer or check writer, which is the person who orders the bank to pay cash from the account.

1, Check number. 2, Date of check. 3, American Bankers Association (ABA) bank identification number. 4, Payee (the person or company to be paid). 5, Amount of check in figures. 6, Amount of check in words. 7, Drawee (the bank on which the check is drawn). 8, Bank identification number magnetically printed for electronic processing. 9, Customer account number magnetically printed for electronic processing. 10, Signature of drawer. 11, Reason check was written.

Preparing Checks

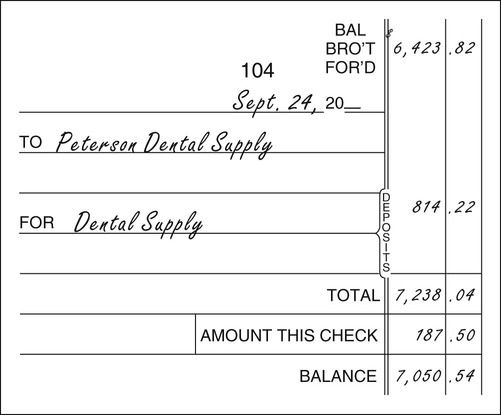

In the past, the administrative assistant prepared checks manually. Today, with the use of financial management software, the assistant can set aside some time during the working day as the schedule permits to prepare the checks with the use of the selected software. If a manual system is used, the following steps are taken when writing the check. The check stub or checkbook register should be completed before the check is written or printed. The stub or register provides a record of the following: (1) the check number; (2) the date; (3) the payee; (4) the amount of the check; (5) the purpose of the check; and (6) the new balance brought forward after the amount of the check has been subtracted. It also provides the new balance if a deposit is to be added to the previous balance, as shown in the manual system (Figure 16-7).

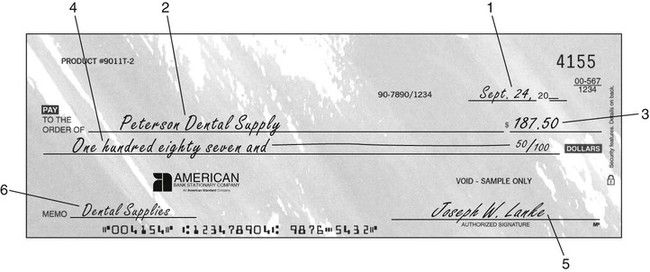

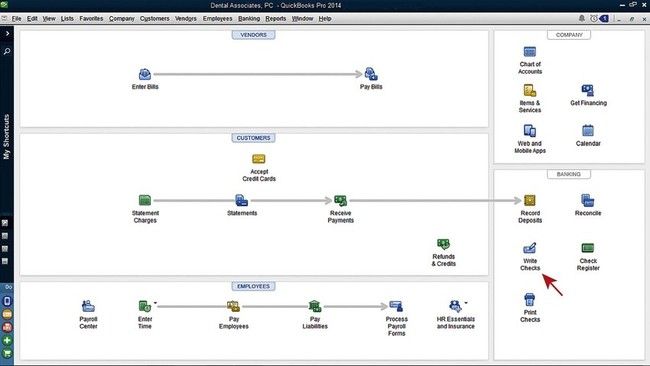

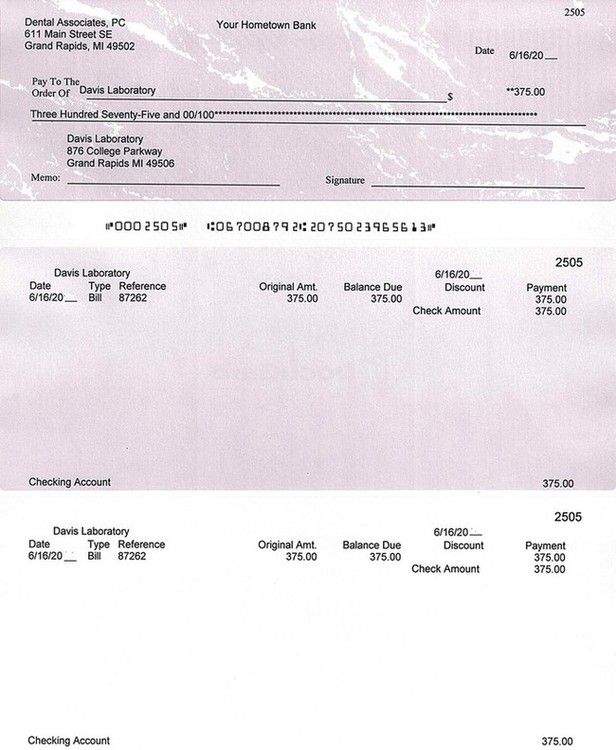

Figure 16-8 presents a step-by-step procedure for manually writing a check. A check produced by a software system such as QuickBooks requires that the user select the icon for check writing from the main screen (Figure 16-9) and then follow through with the data entry as requested on each screen. A check written to a dental supplier includes information important about the check and the account (Figure 16-10).

Types of Checks

The following list describes a few of the types of checks that the administrative assistant may receive:

Stay updated, free dental videos. Join our Telegram channel

VIDEdental - Online dental courses