Chapter 9

Financial Statements

In business a reputation for keeping absolutely to the letter and spirit of an agreement, even when it is unfavorable, is the most precious of assets, although it is not entered in the balance sheet.

Lord Chandos

Family budget

Corporate balance sheet

Corporate profit-and-loss (income) statement

Cash flow statement

Personal balance sheet

Personal income statement

Pro forma statements

2. Describe how each of the financial statements are used in dental practice.

3. Describe cash flow and its importance to the dental practice.

4. Describe working capital and how it is used in a dental practice.

assets

balance sheet

budget

cash flow statement

expenses

financial statements

income

income statement

liabilities

loss

net worth

operating statement

pro forma statements

profit

profit-and-loss statement

statement of financial position

variance

Business has a vocabulary that is as specific and descriptive as any other written or spoken language. Words have meanings in the language of business that business people the world over recognize. The first of those words are the different types of financial statements.

Financial statements are the way that businesses commonly express their financial transactions and history. They take the same, standard format, regardless the type or size of business. In this way, banks and other financial institutions can easily assess financial health and compare one operation to other, similar organizations. Dentists need to understand how to develop these statements, what each component is, and how to use them. Bankers will probably call a dental practitioner to develop each of these forms if he or she requests a loan for practice purchase or start-up.

Two forms of financial statements, personal and corporate, are shown in this chapter. Because most dentists must personally guarantee loans and other practice finance options, bankers generally require a personal financial statement for these guarantees. The proprietor practitioner is inseparable from the practice, so personal statements are especially appropriate for them. With large or networked practices, bankers may request the corporate form of these statements because the personal involvement of a dentist is less critical for their success. The format of the forms is similar, though not exactly the same.

The forms discussed are:

Personal Financial Forms

Personal financial forms show the state of a person’s personal financial health. If a person owns a dental practice, he or she finds it difficult to separate himself or herself financially from the businesses. These financial forms will help to examine that difference.

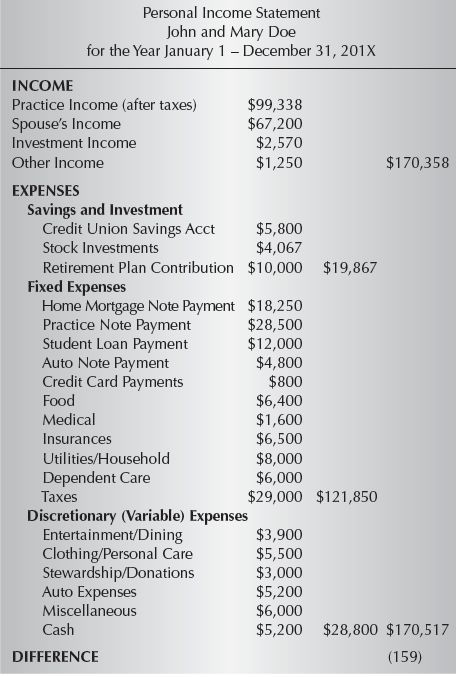

Personal Income Statement

The personal income statement is a moving picture of a person’s personal cash inflows and outflows (Box 9.1). The income statement examines money flows over a specific period, generally a month or year. It is often used as the basis for developing a budget, which aims to use past income and expenditures to plan for the future.

This statement looks at the sources and uses of personal family money. Exact categories of income and expense will be different depending on a person’s personal situation. If, for example, a person is not married, then a spouse’s income is meaningless. If a person is divorced, then a line for alimony or child support payments might be added to the income or expense section (depending on whether a person is paying or receiving these payments).

Expenses are usually grouped by type on the personal income statement. Savings and investments are payments that a person really makes to himself or herself. The payments still represent cash flowing through to the savings or investment vehicle, so they must be accounted for. They then appear on the personal balance sheet, making that statement more positive. Fixed expenses are those that generally cannot be changed over the short term. A person can buy a smaller home, decreasing the payment in the future, but for the immediate concern, a person cannot change a home mortgage payment. (Most debt service is a fixed expense.) A person may have some control over expenses such as food (buying hamburger instead of steak), but he or she still must spend money on these fixed expenses. Discretionary, or variable, expenses are those that a person consciously chooses to make. A person doe not need to go out to a restaurant for dinner. He or she can save money by staying in and cooking, so the dining experience is a discretionary financial decision. (There is obvious personal choice in deciding which of these expenses are discretionary and which are fixed.) The difference between income and expenses tells whether a person is living within his or her means.

Many people use the personal income statement as the beginning point for developing a budget for personal financial planning. A budget is a statement of how a person has spent money in the past and an estimate of future income and expenses. Budgets are used for planning the financial needs of a family by setting expected goals for income or expense by explaining and evaluating spending patterns. As such, they become a target for day-to-day financial living. Budgets are most frequently used when a family is having a financial problem. They then help set targets for spending and let everyone know why spending is limited in one area or another. A budget can help coordinate savings and improve living standards by identifying areas of waste. Bankers may require that a person develops an income statement or family budget when borrowing money to set up or buy out a dental practice. The bank wants to make sure that the person has assessed how much money needed for family living expenses so that the bank can evaluate whether the business can support all of the cash needs (operating, tax, financial, and personal).

Example Personal Income Statement

The sample statement in Table 9.1 shows a personal income statement for John and Mary Doe for the year given. It shows family income from Mary’s practice, John’s work, and other sources. The total of each category is in the next column to the right of the last entry for the category. Family expenses for the Does are broken into three categories: savings, fixed, and variable expenses. In the example statement, John and Mary are close to living within their income. They are making substantial deposits into savings, investments, and retirement plans. Most of their discretionary expenses are well under control, which in turn allows for the high savings rate.

Table 9.1 Example Personal Income Statement

Personal Balance Sheet

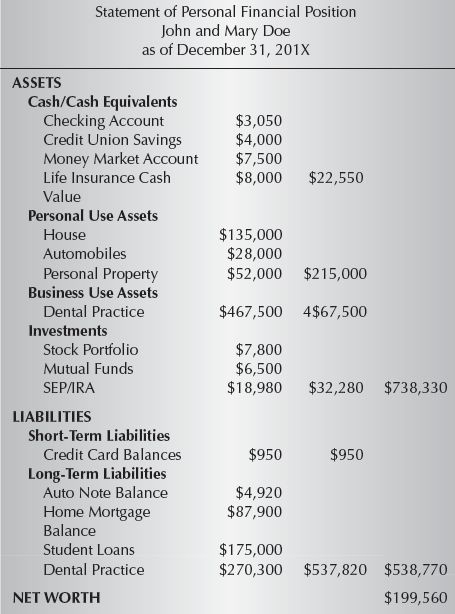

The statement of financial position (balance sheet) shows what a person owns (assets) and what a person owes (liabilities) at a specific point in time. The balance sheet then is a “snapshot” of a person’s financial position at a declared date. It will be different tomorrow as assets change value and as loans are paid off. In fact, bankers and financial planners like to examine changes in a balance sheet to learn how well a person is doing financially. (Total net worth should be growing.)

The balance sheet should become more positive over time. This shows that a person is accumulating wealth and paying off loans. There are really only two ways for net worth to grow (Box 9.2). A person can increase assets by either saving money or increasing the value of an asset. Or a person can decrease liabilities by paying off debt. If a person borrows and then uses the money to purchase an asset, net worth remains unchanged. This happens, for example, when a person buys a dental practice. He or she takes on debt but also now owns an asset of equal value. The net worth remains unchanged. As the debt is paid down or the value of the practice increases, net worth becomes more positive.

It is possible to have negative net worth. This happens to young professionals who have significant educational debt and few assets. Their total liabilities (educational and other debts) are more than the total of what they presently own (assets). Although not an enviable position, it is common.

Bankers generally ask a person to prepare a personal balance sheet when he or she applies for a loan or to borrow money for a business or personal purchase. It is also good practice for the person to prepare one each year to assess his or her financial status. If a person is a proprietor, he or she will use a personal balance sheet (because all assets and debts are personal) and include the practice as an asset on the statement. If a person belongs to an incorporated business, he or she may need to develop two statements, one for the practice (a corporate balance sheet) and the other a personal statement of financial position. Often banks have specific forms that need to be completed. These forms are usually the bank’s particular versions of the generic balance sheet.

Example Personal Balance Sheet

Table 9.2 is a personal balance sheet for John and Dr. Mary Doe. These are things that they own as husband and wife. The balance sheet is for the date given. It will be different as the Does’ investment change value or as they pay off loans or buy new assets. Each type (or class) of asset or liability is grouped together. The value of each asset is in the first column, and the sum of the value of the assets in the class is in the second column, next to the last individual asset value. The assets class values are then summed similarly to develop a total of all assets (in the third column).

Table 9.2 Example Personal Balance Sheet

The first asset class is “Cash” (or items that we can quickly convert that into cash). Cash is needed for routine, daily purchases, and for an emergency. Investments are not considered “near cash” because a person might lose a large portion of his or her value if he or she were forced to sell the investments at the “wrong time.” Personal-use assets are not important from a financial planning perspective. Most people will not sell their house or car when they retire, for example, so these assets are not used for retirement or investment planning purposes. Business-use assets should generate income at a level that gives a reasonable return on the investment. These assets are often sold at retirement and can become a part of the retirement portfolio. The personal balance sheet shows personal items owned and amounts owed. One of those business assets may be a dental practice. Investments are long-term assets that should generate a reasonable return (over time). They become the backbone of retirement, personal, and business planning efforts.

Liabilities are similarly grouped. Short-term liabilities are debts that a person owes that are due in 1 year or less. In Table 9.2, credit card balances are due immediately. This might also include signature loans, bridge loans, or other short-term borrowing. Long-term liabilities are debts that will take more than one (or many) years to pay off. The example shows an auto loan, home mortgage, student loan, and a practice loan. Each of these long-term liabilities should have a capital (or other large) asset on the list for which the liability paid. The auto, home, and dental practice notes are each associated with an obvious asset. The one questionable i/>

Stay updated, free dental videos. Join our Telegram channel

VIDEdental - Online dental courses