Chapter 7

Basic Economics

If you teach a parrot to say “Supply and Demand,” you can get him a Ph.D. in economics.

Thomas Carlyle

composition of GDP

consumer confidence index (CCI)

consumer price index (CPI)

contraction phase

deflation

demand for dental services

apparent price

availability of substitutes

determinants of demand

nonprice considerations

price

discount rate

expansion phase

Federal Reserve System (Fed)

fiscal policy

Federal Open Market Committee (FOMC)

general economic prosperity

primary industries

secondary industries

tertiary industries

government borrowing

government spending

gross domestic product (GDP)

gross national product (GNP)

inflation

laws of economics

economic goods

opportunity cost

private consumption good

public consumption goods

leading economic indicators

market equilibrium

market

market price

market shortage

market surplus

monetary policy

open market operations

recovery phase

reserve requirement

supply and demand

demand

elasticity

demand curve

law of demand

market demand

supply

barriers to entry

elastic supply

law of supply

market supply

supply curve

supply siders

tax law changes

Economics deals with human wants, needs, behaviors, and responses. As such, economists can never “prove” anything. That is, there are always confounding factors in real-life economics that makes all economic ideas “theories” that must applied in individual circumstances.

Dental services respond to the laws of economics like any other good or service. Understanding the basic notions of supply-and-demand economics accurately to respond to changing economic conditions is, therefore, important for practitioners. The study of economics is usually broken into two general areas: macroeconomics and microeconomics. The difference in the two is a difference in scope. Macroeconomics looks at the whole economy and forces that affect it. If forces that affect the entire dental industry, such as national economic policies, changing demographic patterns, bank interest rates, inflation, and labor supply issues, are examined, this is a macro view of economic conditions. Microeconomics looks at the individual business, person, or practice and how he or she responds to changing conditions. It examines how prices are determined, and how much goods and services each individual produces and consumes. Each has major implications for how a person practices dentistry.

Microeconomics: The Individual Buyer and Seller

Microeconomics examines the individual firm (or practice) and individual consumers that purchase goods and services from those firms. It attempts to answer questions of why people buy, at what price they will buy, and what producers are willing and able to do to influence their buying decisions. Several microeconomic theories and their effects on dental practices are described.

Public and Private Goods

Any time economists speak of economic “goods” they refer to anything that is both desirable and limited and for which people will give up something else to obtain. A good may be physical items for sale (e.g., cars, televisions, or shampoo) or services that consumers buy and use immediately (e.g., hair cuts, dance lessons, or massages). In this sense, dentistry sells goods consisting of both the physical products such as dentures, partials, and restorations, and the less tangible service “good” such as prophylaxes, endodontics, whitening procedures, or extractions. Some people even view intangible items such as leisure time and health as goods because people are willing to sacrifice to “buy” these commodities.

Economists often speak of public or private consumption goods. A private consumption good is purchased and consumed by an individual in the society, rather than the whole society. (A whole group may individually purchase and consume the good, but it is not done as an act of the whole, rather as acts of individuals.) When individuals purchase DVD players, vacations, automobiles, and food, they are consuming those goods privately. If a person cannot pay the price required, he or she is excluded from having the use and benefit of the good. Public consumption goods benefit the whole of society, or at least many people. National defense, the road system, and police and fire protection are examples of public goods enjoyed equally by most people in society. Society cannot legitimately exclude those who cannot pay from enjoying the use and benefit of these goods.

Because private suppliers cannot exclude nonpayers from enjoying public consumption goods, they generally will not provide these goods on a for-profit basis. Instead, government is expected to provide public consumption goods. (Government may contract with private suppliers to provide the good or service, but the government is still ultimately responsible.) There is a significant ongoing debate in this country over what a public good is and what level of those services should be provided. Different people believe that health, and therefore medical and dental care, “fit” as either private or public goods. Depending on the answer, a different set of financing, access, delivery, and pricing policies will result.

Presently, US society considers dentistry a private consumption good. People will purchase as much of the service as they want and can afford. Although the government provides some dental services, people do not have unlimited and equal access to the service. Because dentistry is a private consumption good, it follows the economic laws of supply and demand.

Economic Choices

Economists believe that all economic resources are limited. That is to say that everything people use to produce or purchase economic goods and services that they desire are limited or scarce. Because these resources are limited, people are forced to make choices between alternatives that provide satisfaction. The choice not taken is lost, and therefore sacrificed. This sacrifice is called an “opportunity cost.” For example, a family may have a given income. They want to purchase both a new car and a larger home. Because of their income limitations, they cannot purchase both goods (the car and the home). Instead, they are forced to decide between the two. If they choose to buy the car, they lose the enjoyment of the new home (an opportunity cost). However, if they decide to make a down payment on a new home, they forego the satisfaction from the car.

The notion of economic choice applies to both producers and consumers. Different people weigh the values of goods and services, and therefore the opportunity cost of forgoing those goods, differently. A consumer with limited resources may need to decide between a vacation and extensive dental work. The opportunity cost associated with foregoing each option will help to decide. As a producer, a dentist needs to decide the value of economic goods such as leisure and recreational time. Although a person may have the opportunity to make additional income by working longer hours, he or she will weigh the opportunity costs associated with foregoing time for personal and family enjoyment.

Laws of Supply and Demand

The basic issue of economic is choice making. Both society as a whole and individuals within that society decide what to produce and consume. The way that people decide to use their limited resources determines both the supply of and demand for goods and services within a market economy. This free choice leads to the US capitalistic, market-driven economy. Other systems (Communism, and to a degree, Socialism) plan the economy and determine how much of each good and service is provided and at what price.

Demand

To the economist, demand means the quantity of a good or service that individuals are willing and able to buy at each and every possible price. Demand then defines a relationship between price of a commodity and the number of units the buyer is willing to purchase. It implies that consumers both want the product and can pay for it. The resulting law of demand states that “as the price of any good decreases, the quantity of that good that consumers are willing and able to purchase will increase. As price increases, consumers will demand a smaller quantity of the good.” This is an inverse relationship; as one factor gets larger, the other gets smaller. Evidence of this law in action can be seen by looking at everyday buying habits. Clothing stores lower the price at the end of season to clear their racks of goods. Unscrupulous contractors and building suppliers increase prices after a natural disaster, when demand is high. Automobile dealers stimulate demand through rebates and other discount offers.

Demand has the important characteristic of elasticity. A demand that is very elastic means that the quantity demanded (and bought) is sensitive to price. Here, the demand curve is much flatter. For example, as the price of coffee rises, consumers buy less and less coffee, instead buying substitutes, such as tea and colas. Inelastic demand means that the quantity demanded is insensitive to the price of the good or service. For example, diabetics will buy the same amount of insulin despite the price. Their demand for the good is inelastic and the curve is steeper.

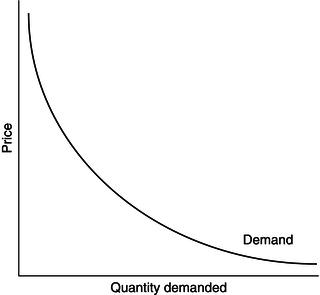

A demand curve is a graphical representation of this relationship between price and quantity demanded. A demand curve can be drawn for any good or service in the market, and the curve always slopes down and to the right. Although many actual demand curves have been determined for various products, they are more useful for understanding the concepts of economics. Figure 7.1 shows a typical, hypothetical demand curve, in this case for crowns. As the price of crowns increase, fewer people are willing and able to afford this service; the quantity demanded then decreases. Any individual buyer will reach a point at which they refuse to buy any additional units because they have fulfilled their needs or because their opportunity costs are too high. Their demand is essentially satiated. However, as the price decreases, more buyers come into the market and are willing to purchase the good, although other consumers may have dropped out of the market.

An individual consumer’s demand for services will vary depending on factors such as income level, future expectations, and personal wants and desires. Demand curves are then generally determined for the entire market. A market demand is simply equal to the sum of all the individual demands. This realizes that some consumers will never buy the product (e.g., gold crowns) at any price, others may buy many products at unlimited price, and most fall onto a continuum between the two extremes.

Figure 7.1 A demand curve

Supply

To this point, only one side of the economic exchange, the buyer, has been looked at. The behavior of the seller or producer (the “supplier”) is equally important to the transaction.

To the economist supply means the quantity of a good or service that the supplier is willing and able to offer for sale at every possible price. Suppliers are usually thought of as the people who own factories, shoe stores, or dental offices. These are the suppliers in the product market for final goods and services. However, there is a similar market for resources to produce the goods. Producers must compete in the open market for wheat for bread, steel for cars, and an hour of the hygienist’s time.

Supply then defines a relationship between price of a commodity and the number of units the seller is willing to supply. The resulting law of supply states that “as the price of any good increase, the quantity of that good that suppliers are willing and able to offer for sale will increase. As price increases, suppliers will supply a larger quantity of the good.” This is a direct relationship; as one factor gets larger, so does the other. Supply displays the characteristic of elasticity similar to demand. Elastic supply means that a change in the price of the good leads to a large change in the quantity supplied.

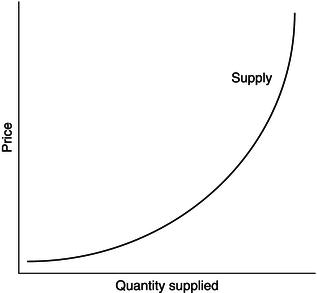

A supply curve is a graphical representation of this relationship between price and quantity supplied. A supply curve can be drawn for any good or service in the market, and the curve always slopes upward and to the right. Figure 7.2 shows a typical, hypothetical supply curve, in this case also for gold crowns. As the price of gold crowns increase, dentists are willing to work harder and produce more of the products; the quantity supplied then increases. Any individual seller will reach a point at which they refuse to produce any additional units because they have fulfilled their needs or because their opportunity costs are too high. Their supply is essentially satiated.

An individual producer’s supply of services will vary depending on factors such as the cost of production, degree of profitability, future expectations, and personal wants and desires. Supply curves are also determined for the entire market. A market supply is simply equal to the sum of all the individual supplies. The market supply is determined largely by the obtainable profits. If supplying the good or service is lucrative compared with other forms of income generation, then more people will attempt to become suppliers. The size of the market, social climate, and barriers to entry limit the numbers of successful suppliers. Dentistry, for example, has steep barriers to entry in that there are academic dental school entrance requirements, limited number of dental school places, licensure requirements, and high start-up costs. These barriers keep the supply curve for dentistry stable.

Figure 7.2 A supply curve

There is little support for the idea that more providers of health services lowers the cost to the public. In fact, the opposite may be the case. It is well established that the number of surgeons in an area determines how much surgery is done in that area. Dentistry may follow a similar pattern. Rather than competition stimulating price reductions, it may increase prices in an area. One explanation for this apparent paradox is that practitioners may need to generate a certain amount of money to meet expenses and have a targeted income for themselves. According to this “target income hypothesis,” fees in an area will increase until practitioners meet those needs.

Market Equilibrium in Demand and Supply

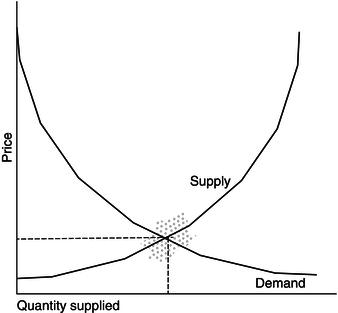

A “market” occurs when suppliers and demanders (consumers) exchange value (money). In a dynamic market, changes are expected to take place in both supply of and demand for services as the underlying conditions change. When the forces of supply interact with the forces of demand, a market price is established, which is an equilibrium point where the supply of goods and the demand for those same goods is equal. Graphically, this occurs where the upward-sloping supply curve and the downward-sloping demand curve intersect (Fig. 7.3).

Figure 7.3 Market equilibrium

A market is never in exact equilibrium. Instead, there is fluctuation as producers and consumers adjust to changing conditions. A market shortage is a condition in which the demand for a good or service is greater than the supply of that good or service. The price then rises as consumers bid up the price. More dollars then chase fewer goods until suppliers produce either more goods or service or more suppliers enter the market (increasing production) to take advantage of excess profits. A market surplus is a condition in which the supply of a good or service is greater than the demand for that good or service. Prices drop as suppliers accept less to sell products. Profits for producers decrease as the price falls. Eventually, inefficient producers are forced from the market as profit margins decrease.

If a good is freely traded, shortages and surpluses do not last. The forces of market competition cause a readjustment of prices and it establishes a new equilibrium. Those who are willing to pay more will get what they want, pushing up prices and eliminating the shortage. Those who are willing to sell for less will gather sales, driving down prices and eliminating surpluses.

Resource markets behave similarly to final goods and services. Businesses become the demanders and households (and the people who make them up) are the suppliers. Dentists compete not only with each other for the services of staff but also with alternative forms of employment. If dentists, as a group, do not pay a wage comparable to similar forms of employment, given similar background, training requirements, and working conditions, then a shortage will occur. This drives the price of staff members up. If an individual dentist wants to hire a hygienist at less than the market rate for hygienists, he or she probably cannot hire one, unless other nonwage factors (e.g., benefits, time off, convenience) balance the hygienist’s opportunity cost of a lower wage.

The Economics of Dental Services

Given that dentistry is a private consumption good, it would be expected to react to the forces of supply and demand in the marketplace as any other consumer good. And in fact, that is what happens. These macro forces occur through an aggregation of individual micro choices. So when thinking about the overall demand for services, more (but not all) of dental patients respond as the macro theory predicts.

Demand for Dental Services

Demand for dental services follows the classic downward-sloping demand curve. However, many social factors affect the shape of the demand curve. These are called the determinants of demand.

Price

Price is, by definition, one primary determinant of demand. Equally important to the true price is the apparent price for the consumer. Third-party plans, in effect, reduce the apparent price to the consumer by 50, 80, or even 100 percent. If a patient’s insurance pays 50 percent, the procedure which in reality costs $300 apparently only costs $150. Cons/>

Stay updated, free dental videos. Join our Telegram channel

VIDEdental - Online dental courses