Banks and other financial institutions use several standard types of statements to assess the financial health of a business. Understanding how to develop these statements, what each component is, and what they show is important. A bank may require the borrower to develop each of these forms when requesting a loan for practice purchase or start-up. The information on these forms can then be used for planning and analysis of the practice.

1. The statement of financial position (balance sheet) shows what someone owns (assets) and what they owe (liabilities) at a specific point in time. The general formula for a statement of financial position is given in Table 3.1. The balance sheet is a “snapshot” of a financial position. It will be different tomorrow, as assets change value and loans are paid off. Bankers and financial planners like to examine changes in the balance sheet to decide how well someone is doing financially. (Total net worth should be growing.) Net worth can grow in two ways. One, assets can increase by savings or through increasing the value of an asset. Two, liabilities can decrease by paying off debt. Borrowing and then using the money to purchase an asset leaves the net worth unchanged. This happens when a new dentist buys a dental practice. He or she takes on debt but also now owns an asset of equal value. The total net worth remains unchanged. As he or she pays down the debt or the value of the practice increases, net worth becomes more positive.

It is possible to have a negative net worth. This happens to young professionals who have significant educational debt and few assets. Their total liabilities (educational and other debts) are more than the total of what they presently own (assets). While not an enviable position, it is frequently encountered.

Bankers often require borrowers to develop a personal balance sheet, and/or a balance sheet for the practice. Generally, if the borrower is a sole proprietor, he or she will use a personal balance sheet (since all assets and debts are personal), including the practice as an asset on the statement. If the practice is incorporated or has multiple owners, each of the owners may need to develop two statements, one for the practice and the other a personal statement of financial position. Often banks have specific forms to complete. These are usually their particular versions of the generic balance sheet.

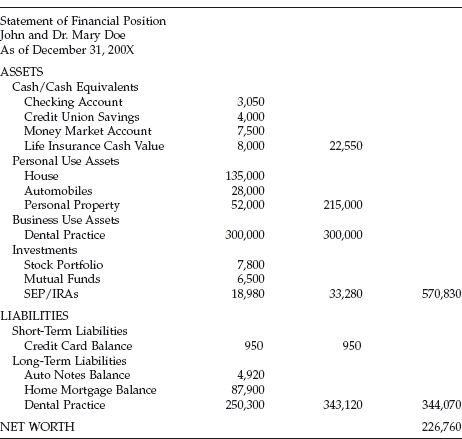

An example balance sheet is shown in Table 3.2. This shows that John and Mary Doe own assets that total $570,830 in value. These assets have been grouped according to their financial use (cash, personal, business, investment) Mary’s dental practice has been valued at $300,000. John and Mary owe a total of $344,070. These debts are categorized by when they will pay them. Short-term liabilities will be paid within a year. Long-term liabilities are loans used to purchase assets that last many years, such as houses, autos, and dental practices. Mary still owes $250,300 on her dental practice, so she has just less than $50,000 of value, or equity, in the practice. The difference between what they own and what they owe is the couple’s net worth, in this case $226,760. This means that if the couple sold everything they own and paid off all their loans, they would have $226,760 in cash remaining.

2. Another statement, called a profit and loss statement, an operating statement, or an income statement, shows income and expenses and the resulting net income or net loss. The general formula for a profit and loss statement is given in Table 3.3. This statement shows a summary of the taxable income and expense items over a specific period. The period may be a day, month, quarter, year, or any other period that gives meaningful information. If the money that flows into the practice is greater than the money that flows out, a profit results. If the outflows are greater, there is a loss. The office checkbook register, whether a manual or computer system, should group expenses according to type. The office management computer system will have income information.

Profit and loss statements may be arranged in two ways, according to their use. (Both contain the same information; they are simply organized differently.) Expenses may be listed alphabetically, which is the same as the format for the tax form Schedule C (Profit or Loss from Operating a Business). Others organize the information by categorizing items of expense. This format makes it easier to do financial analysis on the practice because similar costs (staff, facility, etc.) are grouped together.

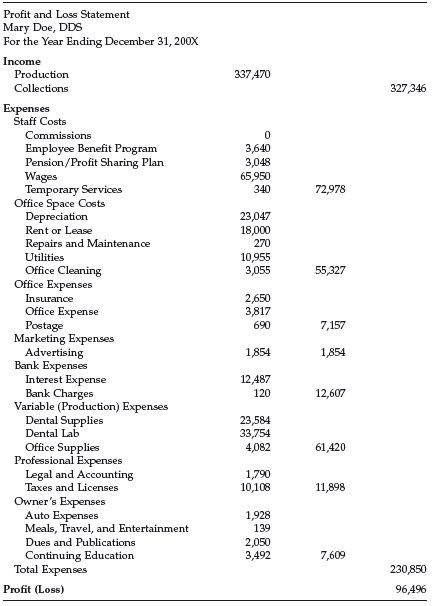

Table 3.4. Example profit and loss statement (Schedule C format).

Profit and Loss (Income) Statement

Mary Doe, DDS

For the Year Ending December 31, 200X

Income

Production

337,470

Collections

327,346

Expenses

Advertising

1,854

Auto Expenses

1,928

Commissions

0

Depreciation

23,047

Employee Benefit Program

3,640

Insurance

2,650

Interest Expense

12,487

Legal and Professional

1,790

Office Expense

3,817

Pension/Profit Sharing Plan

3,048

Rent or Lease

18,000

Repairs and Maintenance

270

Supplies (Office)

4,082

Taxes and Licenses

10,108

Meals, Travel, and Entertainment

139

Utilities

10,955

Wages

65,950

Other Expenses

Temporary Services

340

Bank Charges

120

Office Cleaning

3,055

Dental Supplies

23,584

Dental Lab

33,754

Dues and Publications

2,050

Continuing Education

3,492

Postage

690

Total Expenses/Costs

230,850

Profit (Loss)

96,496

Examples of both types are presented in Tables 3.4 and 3.5. Both show a summary of the income and expenses Mary Doe had in her dental practice for the year ending December 31, 200X. These statements show that Mary produced $337,470 of dentistry during the year. Her practice collected $327,346 in cash, checks, and credit card payments for the year. She uses this number (collections) as the starting point for her profit and loss statement. Her expenses are summarized by item in both forms and grouped by categories in the categorized form. The total cost of $230,850 leaves her a profit of $96,496 for the year. If she had shown a loss for the year, expenses would have been more than income, and the number for the loss would be in parentheses.

Table 3.5. Example profit and loss statement (categorized format).

3. The cash flow statement is primarily a business statement, although we may adapt it to personal situations. The general formula for a cash flow statement is given in Table 3.6. It is similar to a profit and loss statement, with a few important differences. This statement shows the cash receipts and cash disbursements for a specific period and the resulting cash balance changes. The cash flow statement represents changes in the checkbook. The cash flow statement shows the cash changes. The income statement shows tax items. Some transactions involve tax events, but not cash. For example, the income statement lists “depreciation” as an expense. The dentist never wrote a check for depreciation, although he or she claimed it as a tax expense. Some transactions involve cash transfers, but not tax events. For example, if a dentist borrows cash and puts it into a checking account, the dentist has made a cash transaction, although this is not a taxable event. (The dentist does not pay tax on borrowed money. Likewise, when he or she pays back borrowed money to a lender, the principal portion is not a tax deduction, only the interest portion.) Some outflows (such as savings) actually go to you. In reality, savings are an asset that increases on the balance sheet. This improves overall financial position.

Cash flow statements are often used to decide if there is enough money flowing through the practice to make recurring mortgage and other loan payments or other expense items, such as payroll or supplies. We must cover any cash shortage from savings or borrowing. Therefore, cash flow statements must “balance.” That is to say, cash inflows must equal cash outflows.

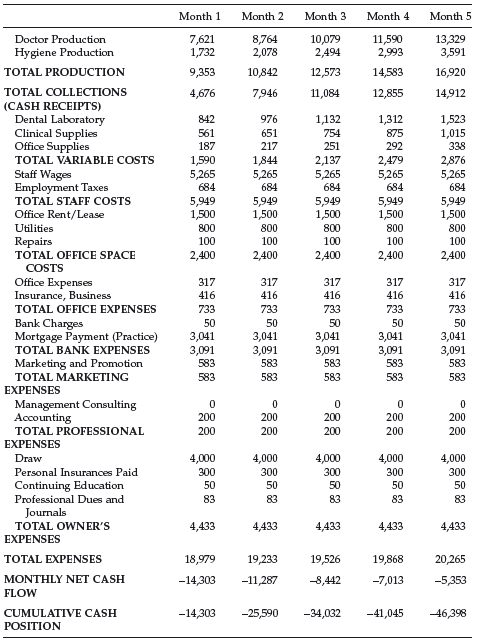

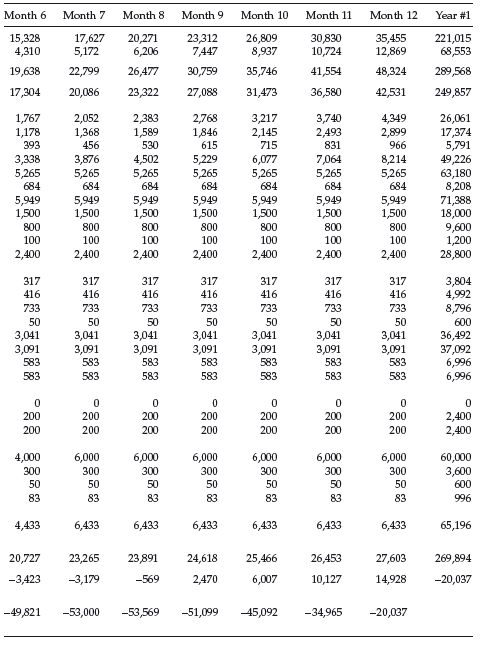

An example of a projected practice cash flow statement is shown in Table 3.7. It shows the projected (estimated) production, collections, and costs by month for the first year of a practice. It includes a mortgage payment each month and a draw or salary for the owner’s living expenses. The line “Monthly Net Cash Flow” shows the anticipated cash flow for the month. The line “Cumulative Cash Position” shows the running total cash excess or shortage. Since the cash inflows must equal cash outflows, this statement shows that the dentist buying into or starting this practice would need to borrow cash to pay the bills until month #9, when monthly net cash flow becomes positive. At this point, there should be enough cash coming through the practice to pay monthly expenses. The maximum amount of cash needed (as working capital) is estimated to be $53,569 in month #8, the largest negative “Monthly Net Cash Flow.” After this point, estimates show the excess cash flow that can be used to pay down the accumulated cash borrowed.

4. A budget is a statement of how money was spent in the past, and an estimate of future income and expenses. The general formula for a budget is given in Table 3.8. As such, a budget becomes a target for day-to-day financial living. Budgets are based on historical evidence. They are used for planning the financial needs of a family or business by setting expected goals for income or expense and by explaining and evaluating spending patterns. The professional budget will help secure professional (office) cash reserves and provide information for expansion or purchase decisions.

Budgets are often used when a family is having a financial problem. They help set targets for spending and let everyone know why spending is being limited in one area or another. A budget can help coordinate savings and improve living standards by identifying areas of waste. A banker may request a family budget to be sure that the practice can support personal income needs without jeopardizing office cash flow.

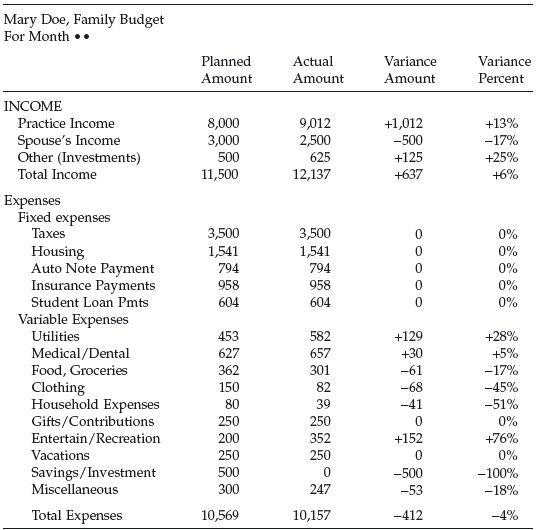

An example of a family budget is displayed in Table 3.9. The family in this example budget came very close to their predicted income and spending patterns. Mary’s income from the practice was slightly higher than expected, which offset her husband’s lower income. Fixed expenses were as expected, because these expenses are preset. Variable expenses were also close to projected. The family had enough money for the month that they could have made a larger savings or investment than planned and still been very close to budget. In future months, they may plan to increase savings. The final chapter of this book also provides information on family budgeting.

5. Pro forma statements are projected statements. They can be any of the four types described above. The essential element of a pro forma is that it is an educated guess of what the statement will be at a given time in the future. For practice statements, this requires estimates of numbers of patient visits, average charges, numbers and pay rates of staff, and many other items of expense. Obviously, a pro forma statement is only as accurate as the educated guess about the future. Often, banks will ask borrowers to develop a pro forma cash flow (to assess whether there is adequate cash to meet expected expenses) and an income statement (to determine your expected income and tax situations).